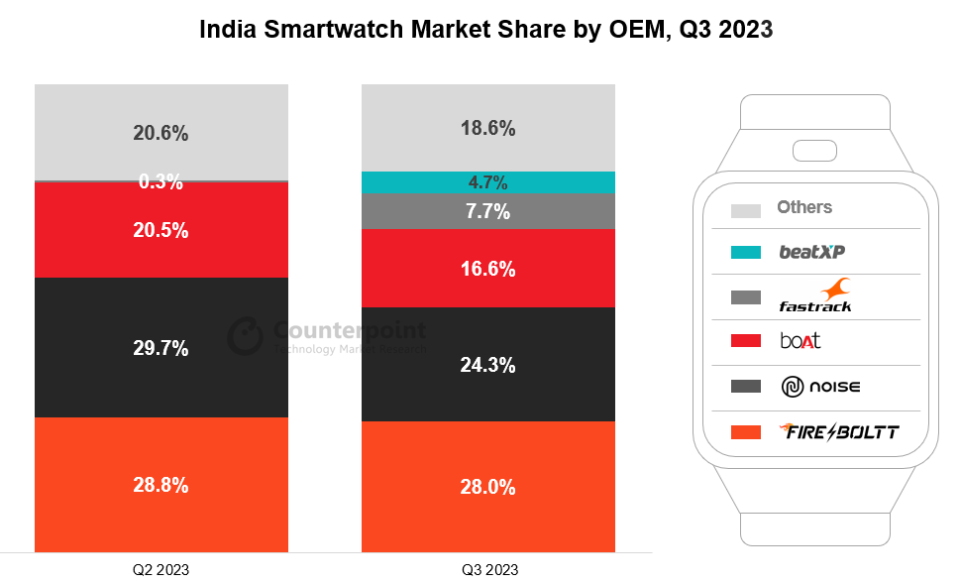

India’s smartwatch shipments grew 21% YoY in Q3 2023 (July-September), according to the latest research from Counterpoint’s IoT Service. The growth was driven by high inventory build-up for the festive season sales in October. While existing top players continued to drive the market, new players like Fastrack and beatXP shipped high volumes and chipped away market share from the top three. The share of domestic manufacturing reached the highest ever at 82%, compared to just 4% a year ago.

Source: Counterpoint’s India Smartwatch Shipments Model Tracker, Q3 2023

Source: Counterpoint’s India Smartwatch Shipments Model Tracker, Q3 2023

Notes: boAt’s share includes Tagg and Defy’s shares; Noise share includes Alt’s share; Figures may not add up to 100% due to rounding“

Commenting on the overall market, Senior Research Analyst Anshika Jain said, “The market reached its highest quarterly shipments in Q3 2023 due to strong festive planning by the brands, new launches, and entry of new players. In this quarter, we saw features like larger screens and OLED displays further trickling down to the lower price bands. As a result, in the INR 2,000-INR 3,000 price band, the contribution of >1.9-inch smartwatches stood at 21%, while over half of the devices were available with OLED displays. In the coming years, the market will continue to grow in double digits due to the brands’ efforts to expand their portfolios, offline partnerships with several large-format retailers (LFRs) and growing emphasis on local manufacturingsource

Commenting on price, Research Analyst Harshit Rastogi said, “Due to continuous push towards budget offerings, India’s smartwatch ASP (average selling price) declined by 41% YoY to reach its lowest-ever level. As a result, over three-fifths of the market now comes under the <INR 2,000 price band. This quarter, smartwatches were even available for less than INR 1,000 to target first-time users. The shorter replacement cycles for the basic smartwatches and the maximum number of new launches being in this price segment further accelerated the trend.”

Market summary

- Fire-Boltt led the market with a 28% share and sported the widest portfolio. It also had the lowest ASP among the top three players, further driving the shipment volume. The Phoenix, Hunter, Ninja Pro Max, Ninja Calling Pro Plus and Ninja Call Pro models drove the market share.

- Noise captured the second spot with a 24% share. The Colorfit Icon 2 was its best-selling model for the quarter. Online channels contributed 79% to its shipments.

- boAt shipments slightly grew YoY. Almost all boAt models are being assembled locally. The brand refreshed several popular models like the Storm Call 2 and Wave Call 2, which were also its bestsellers for the quarter.

- Fastrack, a sub-brand of Titan, an existing giant in traditional watches, captured the fourth spot with an 8% market share. It enjoys an existing brand value, streamlined offline distribution and accessible pricing, facilitating faster growth.

- beatXP entered the top five for the first time after registering 4X QoQ growth in Q3 2023. This fitness-oriented sub-brand of healthcare startup Pristyn Care entered the smartwatch market in Q4 2022. It has more products lined up for the coming quarters and is expected to gain more market share due to its lower ASP.

- Boult grew 251% after entering the offline channel in Q3. The brand has partnered with several LFRs, like Sangeetha Mobiles and Poorvika Mobiles, for better in-store experience and expansion. Corporate sales also remain sizeable for the brand.

- Samsung refreshed its portfolio with sixth-generation smartwatches getting assembled locally. The Galaxy Watch 4 series continues to be Samsung’s bestseller, contributing to 35% of its shipments, primarily due to its comparatively low price. The brand led the INR 10,000-INR 20,000 price band with a 65% share.

- Apple shipments declined by 52% as its new series became available in late September and without a refresh to the Watch SE 2022. The brand remains the market leader in the >INR 20,000 retail price band.

- Around 98% of the smartwatches run on a lighter OS version while the remaining run on a High-Level OS (HLOS), like Wear OS and Watch OS.

Background

Counterpoint Technology Market Research is a global research firm specializing in products in the TMT (technology, media and telecom) industry. It services major technology and financial firms with a mix of monthly reports, customized projects, and detailed analyses of the mobile and technology markets. Its key analysts are seasoned experts in the high-tech industry.